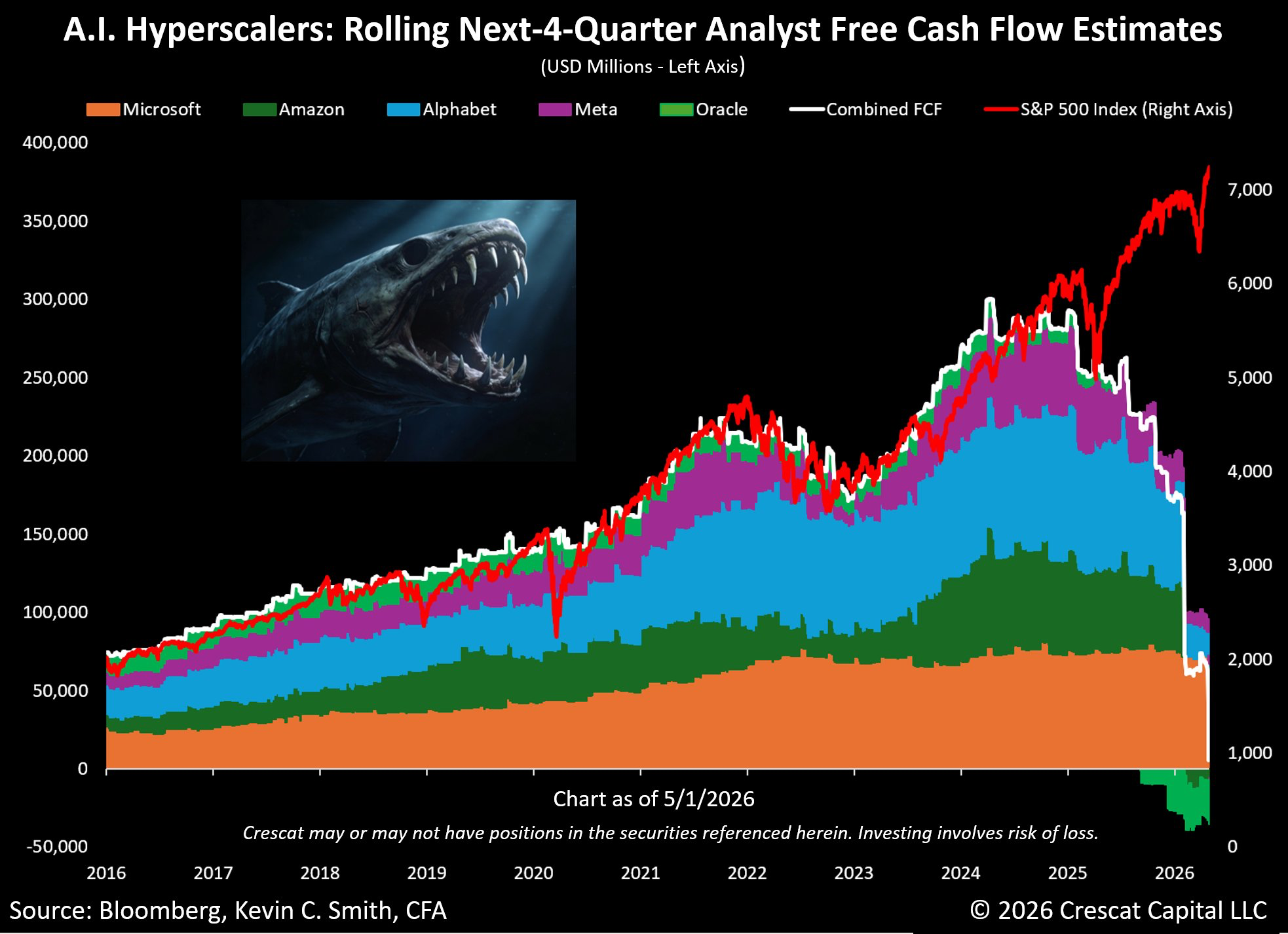

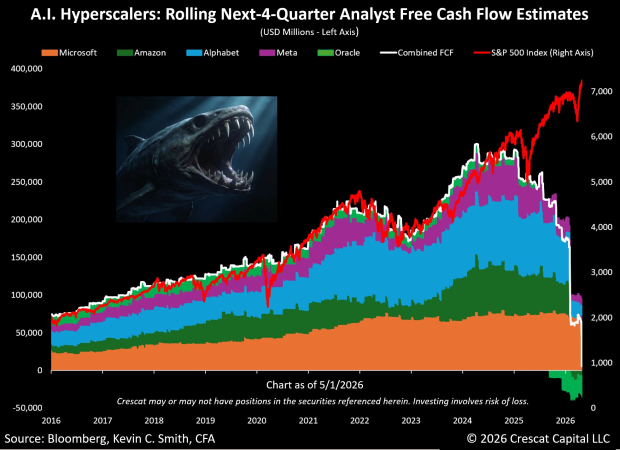

In a striking forecast, Alphabet, Google's parent company, is projected to see its free cash flow (FCF) plummet to zero by 2026. This dramatic shift is primarily attributed to an unprecedented surge in capital expenditures (capex) as the tech giant doubles down on its artificial intelligence (AI) infrastructure.

According to analyst Horace Dediu, Alphabet generated a substantial $73.266 billion in free cash flow in fiscal year 2025. However, this impressive figure pales in comparison to CEO Sundar Pichai's guidance for 2026 capital expenditures, estimated to be in the staggering range of $175 to $185 billion. To put this into perspective, Alphabet's FY2025 operating cash flow was $164.713 billion. If capex hits the midpoint of the guided range, it would essentially consume all the operating cash the business generates, leading to a near-zero FCF.

The Unprecedented AI Spending Spree

The trajectory of Alphabet's capital expenditures reveals an aggressive acceleration. From $32.3 billion in 2023, capex rose to $52.5 billion in 2024, and then surged to $91.4 billion in 2025 – a 74% year-over-year increase. The proposed jump to $175-185 billion in 2026 represents another near-doubling, with Q4 2025 alone seeing a 95% year-over-year growth to $27.9 billion in capex.

This dynamic isn't unique to Alphabet; it's a trend observed across its tech peer group. Amazon, for instance, experienced a similar narrative in 2025, with its FY2025 free cash flow collapsing by 65.95% year-over-year to $11.194 billion as capex reached $131.8 billion. Amazon CEO Andy Jassy has guided for approximately $200 billion in capital expenditures across the company in 2026. Meta and Microsoft are also investing aggressively, with Meta's FY2025 free cash flow declining by 19.39% year-over-year against 2026 capex guidance of $115 to $135 billion, and Microsoft's Q2 FY2026 capex alone hitting $29.9 billion, up 89% year-over-year.

The High Stakes: A "Winner-Take-Most" Game?

The prevailing sentiment among many tech insiders, including Semianalysis CEO Dylan Patel, is that the returns on AI infrastructure will ultimately justify this monumental spend. These businesses, like Alphabet, are not struggling financially; Google Cloud revenue hit $17.7 billion in Q4 2025, up 48% year-over-year, with a 31.6% operating margin at the Alphabet level. From this perspective, the compression of free cash flow is viewed as the "price of admission" for what is believed to be a winner-take-most game in AI infrastructure.

However, skepticism lingers. If the anticipated returns on AI investments do not materialize at the scale management expects, a zero free cash flow for a company with a $1.7 trillion market cap could spark a very different conversation among investors and analysts. The "commodities strike back" theme suggests that the immense investment in underlying infrastructure might eventually lead to commoditization, putting pressure on margins and returns.

Decoding the Financial Implications

Even before these future investments fully impact the balance sheet, Alphabet's trailing twelve months (TTM) Enterprise Value to Free Cash Flow (EV/FCF) ratio has already reached 73, significantly higher than its Price-to-Earnings (P/E) ratio of 29. If FCF indeed goes to zero, the implications for traditional valuation metrics would be profound, challenging how investors assess the company's worth and future prospects.

The Edge vs. Cloud Debate: Monetization Challenges

A critical question revolves around how these hyperscalers will recoup their massive AI investments. While the demand for AI compute currently outstrips supply, concerns arise about future monetization strategies. If AI models become ubiquitous, what mechanisms will these giants employ to charge for their services? And if supply eventually exceeds demand, it could significantly undermine their monetization efforts.

Moreover, a growing debate focuses on the decentralization of AI computation. Some analysts and commentators suggest a potential "mainframe vs. PC" battle, where centralized cloud-based AI (hyperscalers) competes with AI processing at the edge (client devices like PCs, Macs, and smartphones). If much of what companies and individuals need from AI can be performed on in-house computers, the actual money flowing to hyperscalers could be substantially reduced. This "thick client" (edge) approach, akin to how Apple envisions Siri AI, could empower businesses to keep costs internal, potentially limiting the hyperscalers' ability to command premium prices for their services.

Whether the future of AI lies predominantly in the hyper-scale data centers or increasingly at the edge will significantly determine the success of these colossal investments and the ultimate fate of tech giants' free cash flow.